About Us

Who is CUFSS

The majority of Australian Mutual ADI's have established a self-regulatory system "CUFSS Limited" as an additional protection for depositors and in addition to:

- Their long and fine history of forty to sixty (40-60) years of operations;

- Strong capital, and;

- The regulation of the Banking Act and prudential supervision of the Australian Prudential Regulation Authority (APRA).

CUFSS is the Australian Mutual banking industry self-funded and operated "emergency" liquidity support scheme. It is certified by APRA under s11CB of the Banking Act 1959.

CUFSS' objectives are to:

- Protect the interests of member depositors, and

- To promote financial sector stability, particularly in relation to Australian Mutual ADI’s.

CUFSS functions are to:

- Administer the emergency liquidity support system;

- Monitor members' liquidity, capital & profitability;

- Advise members about liquidity and risk management;

- Assist the orderly exit of members by way of merger;

- Determine and arrange emergency financial support if required;

- Liaise closely with regulators.

CUFSS Member's commitment

Each individual CUFSS Member's commitment to the system is through the Industry Support Contract (ISC), which sets out their obligations, rights and responsibilities.

Essentially all parties contractually agree to:

- Provide financial and other information to CUFSS to permit monitoring;

- Fund annual CUFSS operating costs by subscriptions based on member assets, and

- Pledge a contingency commitment of a percentage of assets (currently 3.0%, capped at $100 million) for emergency liquidity support should it be required. Currently close to $1 billion dollars is pledged under the ISC.

As an industry support vehicle, this supervision system is independent from, and additional to, that undertaken by APRA.

The benefits of being a CUFSS member are:

- An extra protection shield for members' own depositors because of the available emergency liquidity support;

- Bolsters members own liquidity risk framework required under APRA Australian Prudential Standards (APS);

- Certified by APRA under the Banking Act (S11CB);

- The CUFSS minimum deposit requirement of 3.0% of assets is exempt from deduction from MLH calculations and entirely controlled by the individual member;

- Members pay only a low annual subscription to fund CUFSS operations;

- CUFSS provides another level of information and access to advice;

- Members are responsible good corporate citizens in being part of an industry wide self funded and regulated liquidity system to protect members.

Background

Background to the formation of CUFSS

CUFSS was established in 1999, by 180 Credit Unions and Cuscal (Note 1) during the transfer to Commonwealth regulation, which replaced statutory provisions under the state-based Financial Institutions (FI) regulatory scheme.

The FI Scheme provided for a system of emergency liquidity and solvency support through the Emergency Liquidity Support Scheme (ELSS) under direction from the Australian Financial Institutions Commission (AFIC), and State-based contingency funds. CUFSS replaced these statutory requirements with a system of self- regulation funded by members, utilising the operational capacity of Cuscal as its banker and that of each member.

Mutual ADI participation in CUFSS and the continuance of an industry support scheme continue to provide a valuable additional protection to Mutual ADI depositors above that afforded by the APRA regulation of the Banking Act.

In addition to the certification of the ISC under the Banking Act, APRA has confirmed that it will recognise membership in the industry support scheme as a factor taken into account, when they assess ADI risk management framework particularly in terms of capital adequacy, liquidity and operational risk.

In the rare circumstances where a CUFSS member requires support beyond that available from their bankers, CUFSS can determine that such support be provided directly from the balance sheets of all participating members. This decision is based on CUFSS review and circumstances.

CUFSS has the capacity to decide whether the support is in the form of a market rate loan, a concessional loan or a permanent loan (the latter category would only be provided in circumstances where a member is to merge or transfer).

CUFSS can and does often provide advice to a member on before or when deciding to provide financial support. Investigations and monitoring processes are included in CUFSS operations.

Background & History

CUFSS decides the terms and conditions applying to financial support. CUFSS’ determination that support should be provided, if accepted by the ‘assisted’ member, will bind all participating members to contribute.

Conditions applying to the provision of support will be stringent and may require the assisted member to appoint an external administrator or cease certain business activities.

A Brief History of CUFSS Limited

- Formed 1999 with 180 Credit Union Shareholders/Members and Cuscal;

- 2004 powers to monitor extended from just liquidity to liquidity, profitability and capital;

- 2007 AGM approved Constitution change to permit “banker of choice” and extend membership potentially to all mutual ADI’s;

- 2008 – ISC invoked with a permanent loan of $839k approved to exit a member, preserve industry reputation risk at start of the GFC. No member deposits lost;

- 2008-2014 Eleven (11) new members joined;

- 2015 ISC varied to reduce members commitments for permanent loans from 0.2% to 0.1% and introduce a maximum cap of $100 million for members 3.0% for non-permanent loans.

- 2016 ISC varied to reduce members’ commitments for permanent loans from 0.1% to 0.00%.

- 2019 Members provided with an Annual Letter of Commitment confirming availability and amount of emergency liquidity support as a percentage of liabilities.

- 2020 ISC varied to include provision of a special loan facility via access to Reserve Bank of Australia funds secured by members internal securitisation securities.

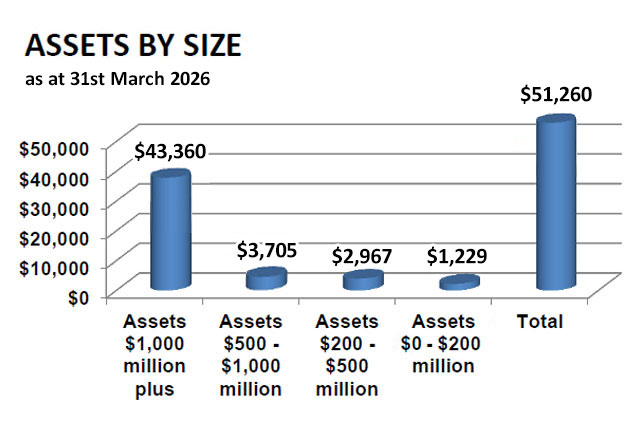

Assets

Assets By Size

as at 31st March 2026

CUFSS Operations

CUFSS has been pro-active in monitoring Mutual ADI performance and where necessary in consulting and conducting reviews and on-site assessments on a number of credit unions, as well as establishing a cooperative relationship with APRA on the monitoring and investigation function which CUFSS performs. CUFSS has an aim to extend coverage to 100% of the Mutual ADI industry.

Profile

A current profile of CUFSS

(as at March 2026)

A Brief History of CUFSS Limited

- 32 Mutual ADI’s (including 11 Credit Unions and 21 Mutual Banks) & Cuscal are shareholders and members;

- CUFSS members have balance sheet assets totaling $51 billion;

- CUFSS is administered by a Board of Directors currently of 4 with a maximum elected by members, 1 appointed by Cuscal and Chair appointed by the directors;

- CUFSS annual operating budget is around $390,000 and funded from levies paid by members according to asset size;

- CUFSS has its own capital/reserves of $294,000;

- CUFSS banker and service provider is Cuscal Limited.

Has the CUFSS emergency liquidity support system been successful?

Well in our view the answer is absolutely because since its formation:

- No depositors have lost deposits or the interest due on them;

- No Mutual ADI liquidations or adverse reputation media stories about Mutual ADI safety have occurred;

- Early consultation between many Mutual ADI's & CUFSS has worked to successfully resolve issues or facilitate voluntary mergers that has protected member deposits and interests and even strengthened member access to banking services;

- Financial assistance has only ever been approved once under the ISC in twenty six (26) years of operation resulting in the transfer of business of a member to another member and no reputation risk to the Mutual ADI industry;

- Close consultation has existed between CUFSS, APRA, Cuscal and Mutual ADI's;

- Quarterly statistical reporting and other consultation has helped all member ADI's in understanding industry and individual trends and in making better decisions for their organisations.